What Insurance Won't Tell You About Water Claims

Your adjuster seems thorough — but their “comprehensive” inspection just missed thousands in hidden damage you're entitled to claim.

Key Takeaway

Insurance companies use specific tactics to minimize water damage payouts. Knowing these strategies and your rights helps you pursue a claim that reflects the full scope of your loss.

Your insurance adjuster just walked through your flooded basement, clipboard in hand, taking photos and making notes. They seem thorough, professional even. But here's what they're not telling you: that “comprehensive” inspection just missed thousands of dollars in hidden damage that you're entitled to claim.

Insurance companies profit when they pay out less than they collect in premiums. While adjusters aren't necessarily trying to cheat you, they're working within systems designed to minimize payouts. Understanding these industry secrets can mean the difference between a $5,000 settlement and the $25,000 restoration your home actually needs.

Insurance Water Damage Claims Tips

The insurance industry operates on a simple principle: pay as little as possible while staying within legal boundaries. This doesn't make them evil, but it does make them profit-driven businesses. Here's what industry insiders know that homeowners typically don't.

Most adjusters are trained to look for obvious damage first. They'll document the standing water, the soaked carpet, the warped baseboards. But they're not incentivized to hunt for problems that might cost their company more money.

“Aaron and his BestDry Team are true professionals — they really care for those they're helping as well as for their industry partners. In a service category where it's hard to know who to trust, this team is the real deal!”

— Nathan Kelly

What Insurance Covers for Water Damage

Standard homeowner's insurance typically covers “sudden and accidental” water damage — burst pipes, appliance malfunctions, and roof leaks from storms. However, the definition of “sudden” is where many claims get disputed.

Insurance companies will investigate whether the damage was truly sudden or if it resulted from gradual deterioration. A pipe that bursts due to freezing is covered. The same pipe that fails due to years of corrosion might not be.

The 72-Hour Documentation Window

Here's something most homeowners never hear: you have roughly 72 hours to document everything before mold growth and secondary damage complicate your claim. After this window, insurance companies can argue that some damage resulted from your delayed response rather than the original incident.

Professional water restoration companies understand this timeline. We've completed over 1,000 projects and know that immediate documentation and mitigation protect both your property and your claim value.

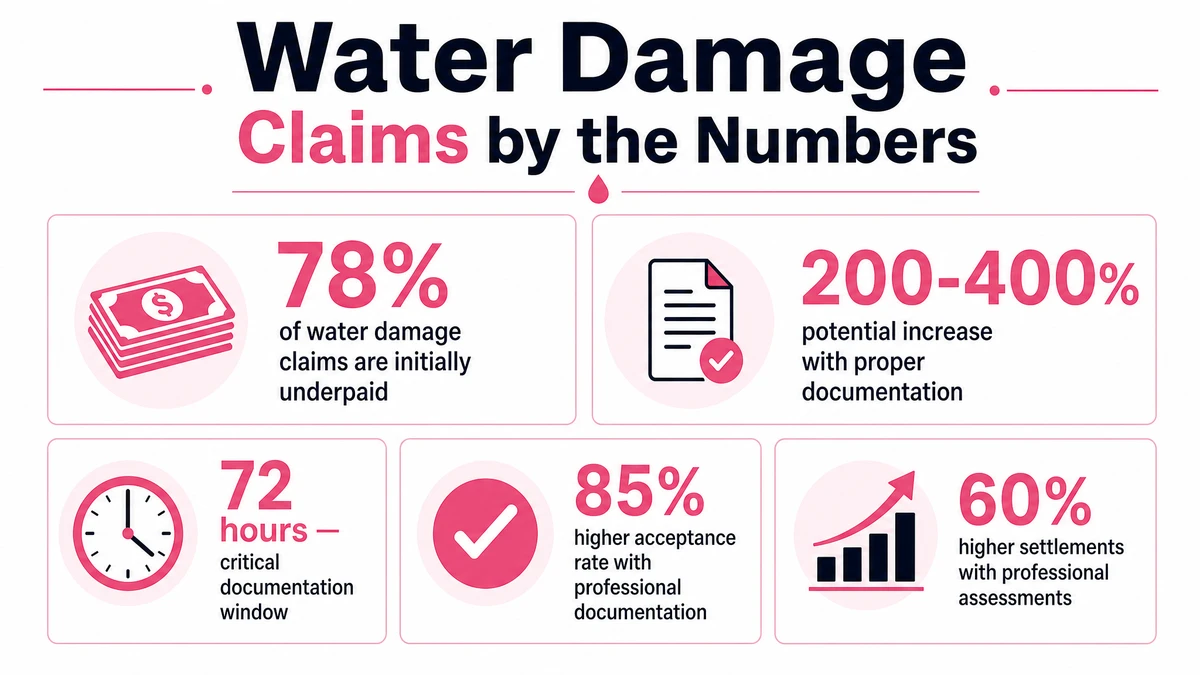

Key water damage insurance claim statistics every homeowner should know

Hidden Damage Insurance Companies Hope You Miss

Insurance adjusters typically spend 30–45 minutes inspecting water damage. That's barely enough time to document obvious problems, let alone discover hidden issues that might not surface for weeks.

Moisture Behind Walls and Under Flooring

Water travels. It seeps behind drywall, under subflooring, and into wall cavities where it can cause structural damage and mold growth. Standard adjusters don't carry moisture meters or thermal imaging equipment to detect this hidden damage.

Professional water restoration specialists use advanced moisture detection equipment to map the full extent of damage. This technology often reveals damage areas 2–3 times larger than what's visible to the naked eye.

HVAC System Contamination

When water damage occurs, contaminated air often circulates through your HVAC system. Ducts can harbor mold spores and bacteria, requiring professional cleaning or replacement. Most insurance adjusters won't even inspect your HVAC system unless you specifically request it.

of water damage claims are initially underpaid according to public adjuster data

The “Scope Creep” Strategy

Insurance companies train adjusters to write narrow scopes of work. They'll approve drying the visible areas but exclude related work like removing unaffected materials to access hidden damage.

Professional restoration follows industry standards that often require removing apparently undamaged materials to properly dry and restore affected areas. This is where the gap between insurance estimates and actual restoration costs becomes apparent.

Material Matching and Depreciation Games

Your 10-year-old hardwood floors are damaged beyond repair. Insurance offers to pay for similar flooring, minus depreciation. But “similar” rarely means identical, and depreciation calculations can be surprisingly aggressive.

Many policies include “matching” clauses that require insurance to replace enough material to achieve a uniform appearance. This often means replacing more flooring, paint, or fixtures than the adjuster's initial estimate suggests.

Timing Tactics That Cost You Money

Insurance companies understand that time pressure works in their favor. The longer your home sits damaged, the more likely you are to accept a quick settlement rather than pursue a claim that reflects the full scope of your loss.

The “Emergency Mitigation” Trap

Most policies require you to mitigate damage immediately to prevent further loss. But insurance companies often dispute mitigation costs that exceed their pre-approved amounts. This creates a catch-22: mitigate quickly and risk non-payment, or delay mitigation and risk claim denial for failure to prevent additional damage.

Working with restoration professionals who understand insurance requirements helps navigate this challenge. As members of PHCC Washington, we know how to document emergency mitigation work clearly and thoroughly.

Documentation That Insurance Companies Don't Want You to Have

The quality of your documentation directly impacts your settlement amount. Insurance companies prefer limited documentation that supports minimal payouts.

Professional Moisture Mapping

Detailed moisture maps showing the full extent of water penetration provide undeniable evidence of damage scope. These maps often reveal affected areas that adjusters miss during quick visual inspections.

Time-Stamped Photo Evidence

Photos taken immediately after damage occurs carry more weight than those taken days later. Insurance companies can argue that delayed photos show additional damage from poor maintenance.

Third-Party Assessments

Independent assessments from certified restoration professionals provide objective evaluations. These reports often identify issues that insurance adjusters overlook or minimize.

Key Takeaway

Professional documentation gives your insurer a clearer, more accurate picture of the loss than homeowner-only documentation.

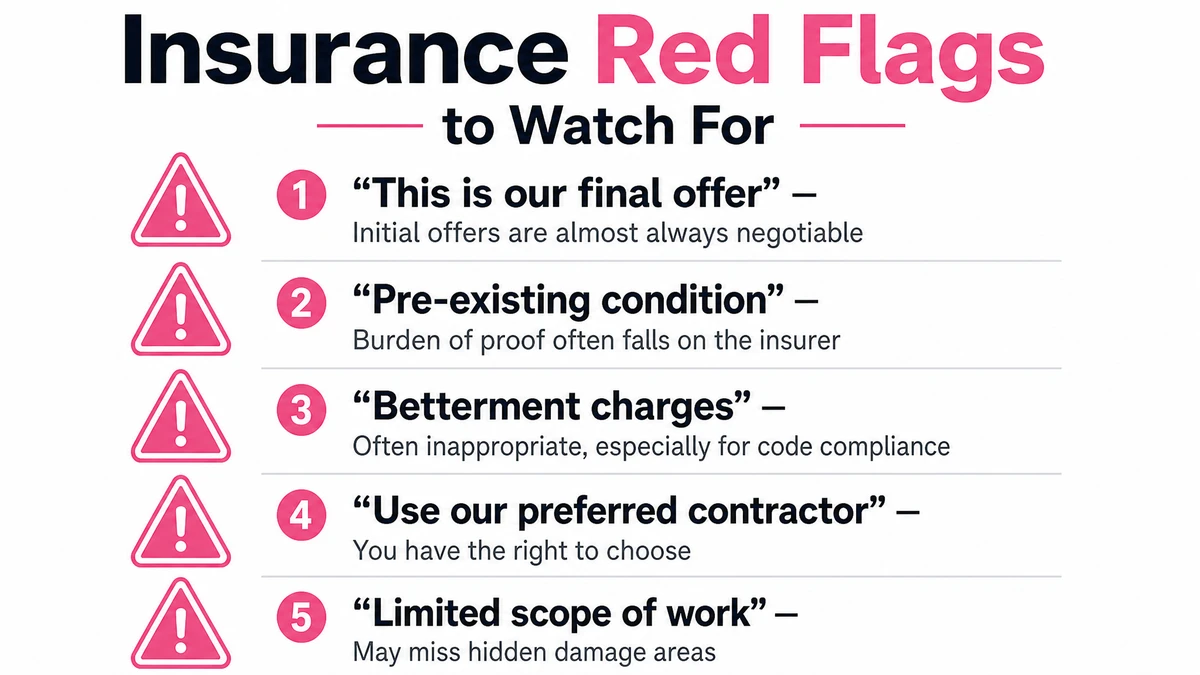

Know these red flags to protect your water damage claim

The Claims Process Manipulation

Insurance companies have refined their claims processes to discourage maximum payouts through procedural complexity and strategic delays.

Multiple Adjuster Strategy

Large claims often involve multiple adjusters: one for structure, one for contents, one for additional living expenses. This fragmentation makes it difficult to see the full scope of coverage and creates opportunities for items to fall through the cracks.

Preferred Contractor Networks

Insurance companies maintain networks of “preferred” contractors who agree to work within predetermined pricing structures. While these contractors may be competent, their primary loyalty is to the insurance company that provides steady work, not to achieving the best outcome for your property.

Your Rights That Insurance Companies Downplay

Insurance policies are contracts, and you have specific rights under these contracts that companies prefer you don't fully understand.

Right to Choose Your Own Contractor

You're not required to use insurance company preferred contractors. You have the right to hire any licensed, insured contractor you choose — including getting your own estimates and challenging insurance company estimates.

Right to Dispute Settlements

Initial settlement offers are often negotiable. You have the right to dispute coverage decisions, request re-inspections, and provide additional documentation to support your claim.

Right to Hire Public Adjusters

Public adjusters work for you, not the insurance company. They can re-evaluate your claim and negotiate on your behalf. While they charge fees (typically 10–15% of settlement increases), they often recover significantly more than their fees cost.

“Thank you Aaron for everything you and your company did to fix my water leak problems. You are clearly a cut above.”

— James Clague

Red Flags in Insurance Company Communications

Certain phrases in insurance communications signal attempts to minimize your claim. Recognizing these red flags helps you respond appropriately.

"This is Our Final Offer"

Insurance companies often present initial offers as final to discourage negotiation. In reality, most settlements are negotiable, especially when you provide additional documentation or expert opinions.

"Pre-Existing Condition"

This phrase appears when insurance companies want to exclude damage by claiming it existed before the covered incident. Pre-existing condition claims require proof, and the burden of proof often falls on the insurance company, not you.

"Betterment" Charges

Insurance companies may claim that repairs improve your property beyond its pre-loss condition and charge you for this "betterment." Many betterment charges are inappropriate, especially when repairs simply bring your property up to current building codes.

Working with Professional Restoration Services

Professional restoration companies provide thorough documentation throughout the insurance process. With 20 years of experience and over 1,000 completed projects, we understand how to document damage and present it clearly and accurately.

Our team includes specialists in water remediation, mold removal, and leak detection who know industry standards and insurance requirements. We provide detailed documentation, moisture mapping, and professional assessments that give your insurer an accurate picture of the loss.

The Claims Concierge Advantage

Our documentation and guidance service provides thorough documentation and helps you understand the claims process. We're mitigation and mold specialists, not public adjusters.

This service gives you clear, thorough documentation and honest guidance for your water damage restoration needs. Coverage decisions are between you and your insurer.

Frequently Asked Questions

How long do I have to file a water damage claim?

Most policies require prompt notification, typically within 24-48 hours of discovering damage. However, you generally have up to one year to file the actual claim paperwork. Document damage immediately and contact your insurance company as soon as possible.

Can insurance companies require me to use specific contractors?

No, insurance companies cannot require you to use their preferred contractors. You have the right to choose any licensed, insured contractor. However, if you choose a more expensive contractor, you may be responsible for costs exceeding the insurance company’s approved amount.

What should I do if my claim is denied?

Request a written explanation for the denial and review your policy carefully. You can dispute the denial by providing additional documentation, requesting a re-inspection, or hiring a public adjuster. Many denials are overturned on appeal with proper documentation.

How do insurance companies determine depreciation on damaged items?

Depreciation calculations vary by item type and age. Insurance companies use industry guides and software to calculate depreciation, but these calculations can be challenged with evidence of actual item condition and replacement costs.

Should I accept the first settlement offer?

First offers are often low and negotiable. Review the settlement details carefully, compare them to professional estimates, and consider whether all damage has been identified. You can negotiate or provide additional documentation to support a higher settlement.

What's the difference between replacement cost and actual cash value coverage?

Replacement cost coverage pays to replace damaged items with new items of similar quality. Actual cash value coverage pays replacement cost minus depreciation. Replacement cost coverage typically provides better protection for significant losses.

How can I prove the extent of hidden water damage?

Professional moisture detection equipment, thermal imaging, and detailed documentation provide proof of hidden damage. Professional restoration companies can provide moisture maps and damage assessments that support comprehensive claims.

Don't Let Insurance Companies Minimize Your Claim

Contact BestDry today for professional water restoration services and documentation and guidance support. Our experienced team documents your loss thoroughly and helps you understand the process while protecting your home from further damage.